Pfizer IncPFE, one of the world’s largest pharmaceutical firms, is on the verge of a bullish Golden Cross, a significant technical indicator suggesting potential upward momentum for the stock.

Currently, PFE stock is trading at around $30, showing a year-to-date gain of 2.6%, despite being down 16% over the past year.

The golden cross, where the short-term moving average crosses above the long-term moving average, is viewed by traders as a bullish signal.

Benzinga

Chart created using Benzinga Pro

Pfizer’s share price is above its 5, 20, and 50-day exponential moving averages, indicating a strong bullish trend. Specifically, PFE stock is trading above its 8-day simple moving average of $29.04, 20-day SMA of $28.35, and 50-day SMA of $28.37, all suggesting bullish pressure.

Benzinga

Chart created using Benzinga Pro

Additionally, Pfizer’s Moving Average Convergence Divergence (MACD) indicator stands at 0.35, reinforcing the bullish outlook, although the Relative Strength Index (RSI) at 68.96 suggests the stock is nearing overbought territory.

Bollinger Bands further support the bullish sentiment, with the 25-period bands ranging from $26.73 to $29.45, with the stock trading over the upper bullish band.

Read Also: Pfizer And Roche Advance On Their Weight Loss Drug Journeys

Looking ahead, Pfizer is anticipated to potentially exceed its financial guidance, driven by higher utilization of its products such as Comirnaty and Paxlovid, and strong performance from its newly acquired oncology portfolio from Seagen.

Analysts forecast up to 30% growth in its oncology franchise and vaccine sales, contributing to Pfizer’s ambitious goal of adding $25 billion in risk-adjusted revenue by 2030.

However, challenges remain. Demand for Pfizer’s COVID-19 products and oncology drugs could fall short of expectations, and risks related to key product sales, pricing pressure, and pipeline developments persist.

Despite these concerns, the upcoming golden cross and recent bullish signals suggest Pfizer stock may be poised for further gains.

As Pfizer prepares to report its Q2 earnings, all eyes will be on whether these bullish indicators translate into sustained growth for the pharmaceutical giant.

Read Next:

Pfizer, Cisco, Arch Capital And More: CNBC’s ‘Final Trades’

Investors are closely watching stocks that could be impacted by the outcome of the Nov. 5 U.S. presidential elections, especially those more exposed to government policy actions such as banking and clean energy.

While U.S. President Joe Biden and Republican presidential candidate Donald Trump are locked in a close election rematch, a two-day Reuters/Ipsos poll showed that Trump had opened a marginal lead in the race to the White House after surviving an assassination attempt.

Here is a list of stocks and sectors that are likely to be impacted if either Trump or Biden serve a second presidential term:

FINANCIALS

UBS analysts are accounting for the prospect of less stringent capital and liquidity rules, and easing financial regulation under Trump's second term as U.S. president, potentially benefiting the banking industry.

Banks, including JPMorgan & Chase JPM, Bank of America BAC, Wells Fargo WFC, Discover Financial DFS, KeyCorp KEY and Synchrony Financial SYF, are seen as some of the likely winners by the brokerage.

CRYPTO AND BLOCKCHAIN-RELATED COMPANIES

Crypto stocks are expected to benefit from Trump's re-entry into the White House as he is widely seen as being crypto friendly.

Stocks, including Coinbase COIN, Marathon Digital MARA and Riot Platforms RIOT, have surged tracking gains in bitcoin after a failed assassination attempt on the former president raised his odds of winning the elections in November.

U.S. regulators have cracked down on the industry with a slew of federal enforcement actions under the Biden administration.

SOLAR STOCKS

J.P.Morgan analysts see risks to spending on green energy under a new Trump administration, which is expected to focus more on maximizing fossil fuel output instead of fighting climate change.

UBS expects incentives for solar manufacturers such as First Solar FSLR, NextEra Energy NEE and Sunrun RUN to stay if Biden is re-elected.

CLEAN ENERGY AND OIL COMPANIES

Biden has made protecting the environment a core part of his economic plans.

Continued support for electrification and clean fuel production under a Biden administration could boost stocks such as Eaton ETN, Quanta Services PWR, Tesla TSLA and Air Products and Chemicals APD, according to UBS.

Existing incentives from the present government will continue to drive advantages for energy-efficient product manufacturers such as Johnson Controls JCI and Trane Technologies TT, as well as waste management companies with recycling infrastructure such as Waste Management WM and Republic Services RSG.

However, increased oil and natural gas investment, more drilling activity and higher natural gas exports could benefit producers such as Exxon Mobil XOM, Cheniere Energy LNG and ConocoPhillips COP under Trump 2.0.

DOMESTIC MANUFACTURERS

Both men have broadly used tariffs to protect the U.S. industry. A new Trump administration is expected to be much more protectionist in terms of import tariffs as he has proposed putting a 10% duty on all imports.

As president, Trump started a tariff war with China and as a candidate this year the Republican nominee has suggested he would impose tariffs of 60% or higher on all Chinese goods. Biden has largely kept his predecessor's tariffs in place, and ratcheted up others.

"The consumer discretionary sector is exposed in that environment," UBS analysts say.

U.S. tariffs on Chinese imports could help domestic manufacturers, namely legacy carmakers Ford F and General Motors GM and steel producers such as Nucor NUE and Steel Dynamics STLD, UBS analysts say.

TRUMP-RELATED STOCKS

Investors expect stocks linked to Donald Trump to move in tandem with the chances of his winning the presidency. These include Trump Media & Technology DJT, in which the former president owns a majority stake, software firm Phunware PHUN and video-sharing platform Rumble RUM.

PRISON OPERATORS

U.S. prison operators such as Geo Group GEO and CoreCivic CXW may benefit from Trump's re-election, on promises of a crackdown on illegal immigration and restrictions on legal immigration, which could boost demand for detention centers.

PHARMACEUTICALS AND INSURERS

UBS sees a lower risk of drug price cuts and an inclination towards Medicare Advantage in a Republican-dominated government, potentially helping drugmakers Eli Lilly LLY and Merck MRK, as well as health insurers such as Humana HUM and UnitedHealth UNH.

Control on drug prices was implemented under the sweeping Inflation Reduction Act by Democrats and Biden.

M&A-RELATED BENEFICIARIES

Trump may take a more lenient approach to antitrust regulation enforcement, according to J.P.Morgan analysts.

UBS expects banks such as Goldman Sachs GS, Morgan Stanley MS, Lazard LLAZ and Evercore EVR, which benefit from M&A activities, to gain from such a policy change.

SEMICONDUCTOR MANUFACTURING

Given the fierce competition with China on semiconductors, UBS expects a second Trump government to drive support for domestic semiconductor manufacturers including Applied Materials AMAT, KLA Corp KLAC, Intel INTC and Texas Instruments TXN.

AGRICULTURE

With the likelihood of more tariffs on Chinese imports under Trump, farmers are expected to receive more federal assistance for lost exports amid a potential trade war. These initiatives could help agricultural equipment makers and suppliers such as Deere and Co DE and Tractor Supply Company TSCO, UBS analysts say.

June 28 2024

7 Stocks, 5 ETFs Move On Friday As Fed's Preferred Inflation Rate Hits 3-Year Low

Futures on U.S. equity indices inched slightly higher in Friday premarket trading after the Fed’s favorite inflation gauge, the Personal Consumption Expenditure (PCE), fell to 2.6% year-on-year in May, as expected.

It marked the lowest inflation rate since March 2021, bolstering market expectations for upcoming Fed interest rate cuts.

After the PCE price index report, traders increased their wagers on a September rate cut, assigning a 68% chance according to CME Group’s FedWatch tool.

Restricting the screener to stocks with a market cap above $50 billion, here are the top performers following the PCE price index report, according to Benzinga Pro.

On Thursday, 2seventy Bio Inc. TSVT completed the asset purchase agreement with Novo Nordisk A/SNVO.

Under the terms, Novo Nordisk has acquired the Hemophilia A program and rights to 2seventy’s in vivo gene editing technology outside of oncology and gene editing for autologous or allogeneic cell therapies of immune cells for autoimmune disease.

The 2seventy bio team currently involved in the program will join Novo Nordisk and continue to advance the technology.

The program is based on the original research agreement, established in 2019, which focused on a gene editing therapy for Hemophilia A.

2seventy bio will focus exclusively on the commercialization and continued development of Abecma(idecabtagene vicleucel), its BCMA-targeted CAR T cell therapy for multiple myeloma, in collaboration with Bristol Myers Squibb & CoBMY.

“We are pleased to announce the completion of this APA with Novo Nordisk as we believe it will provide the appropriate resources for both the team and the science behind this important program,” said Chip Baird, CEO, 2seventy bio.

Under the terms of the agreement, 2seventy will potentially receive payments of up to $40 million.

2seventy will transfer the Hemophilia A program to Novo Nordisk, and the existing collaboration agreement will be terminated.

Additionally, the divestiture will include the transfer of 2seventy Bio’s megaTAL technology and a license to the underlying intellectual property.

Eikon search string for individual stock moves:STXBZ

Wall Street slipped on Monday as wary investors steered clear of risky assets ahead of a key inflation reading and a meeting of the Federal Reserve this week, which could provide clues on the central bank's policy-easing path over the next few months.

At 12:04 ET, the Dow Jones Industrial Average DJI was down 0.06% at 38,775.82. The S&P 500 SPX was up 0.13% at 5,353.7 and the Nasdaq Composite IXIC was up 0.28% at 17,181.094.

The top three S&P 500 (.PG.INX) percentage gainers:

** Southwesy Airlines , up 8.4%

** Constellation Energy Ord , up 7.3%

** Vistra Corp Ord , up 6%

The top three S&P 500 (.PL.INX) percentage losers:

** Huntington Bankshare , down 6%

** Illumina Inc , down 4.5%

** Dayforce Inc Ord , down 3.8%

The top three NYSE (.PG.N) percentage gainers:

** Texas Pacific Land Crp Ord , up 22.6%

** Ivanhoe Electric Ord , up 20.8%

** Idaho Strategic Resources , up 14.8%

The top three NYSE (.PL.N) percentage losers:

** Logistics Properties of America Ord , down 39.8%

The Nasdaq 100 NDX gained 53.31 points, or 0.28%, to 19,054.26 and recorded 5 new highs and 2 new lows. 47 stocks rose and 54 fell as declining issues outnumbered advancers by about a 1.1-to-1 ratio.

All three major U.S. stock indexes green; Dow leads

Financials up most among S&P sectors; real estate is the laggard

Euro STOXX 600 index off ~0.1%

Gold plunges >2%; Dollar, bitcoin, crude rise

U.S. 10-Year Treasury yield jumps to ~4.43%

CRANKING IT UP TO 11: A JOBS REPORT DRILL-DOWN

The Labor Department's hotly anticipated May employment report was reminiscent of a surprise-packed piñata, bursting at the seems with the unexpected.

The report sent yields bounding higher, on lowered rate cut expectations.

To begin with, the U.S. economy added 272,000 jobs last month (USNFAR=ECI), notching a whopping 64.8% increase over April and landing 87,000 jobs north of consensus.

The number marks the ninth upside surprise over the last 12 months and the eighth reading above 200,000 over the same period.

Digging down, service providing jobs accounted for 89.1% of the 229,000 increase in private payrolls, while the government headcount grew by 43,000.

"This is a strong report, and it suggests that there are no signs of any cracks in the labor market," says Peter Cardillo, chief market economist at Spartan Capital Securities. "It's a plus for the economy and for corporate earnings but it's a negative in terms of the prospects of a rate cut perhaps as early as September."

The most eagerly awaited element of this report was average hourly wage growth, which delivered a hotter-than-expected 0.4% monthly increase and edged up to 4.1% year-on-year, snapping a three-month cooling trend.

It's the first major inflation print for May, and while the consumer likely doesn't mind the extra money in their pocket, it's bad news for rate cut watchers.

It tossed cold water on remaining hopes that Powell & Co will implement its first policy rate cut as soon as July.

"The employment and wage gains will generate a pop in aggregate earnings for workers and this should drive a rebound in consumer spending," writes Kathy Bostjancic, chief economist at Nationwide. "This in turn could help keep inflation more buoyant and delay Fed rate cuts to later this year or into next year."

The market is now pricing in an 8.8% likelihood of that happening, down from 21% on Thursday. Odds are nearly 50/50 that the first cut will arrive in September, according to CME's FedWatch tool.

Next, the jobless rate (USUNR=ECI) brought its own surprise to the party by unexpectedly increasing from 3.9% to 4.0%, the highest level since January 2022.

That's quite a trick, considering the fact that the labor market participation rate actually shed 20 basis points to 62.5%.

In the household survey, 250,000 Americans left the workforce entirely, while the ranks of the unemployed grew by 157,000.

But is that good or bad news?

"Higher unemployment could signal weaker wage growth ahead, softer consumer demand, and less pricing power for businesses, which would cool inflation," says Bill Adams, chief economist at Comerica Bank.

"Most Fed policymakers will see May’s strong payrolls growth and uptick in earnings as a sign that immediate rate cuts are not necessary," Adams adds.

Breaking unemployment down by duration, those who have been jobless for longer accounted to a growing slice of the total pie, supporting the growing likelihood - as evidenced by Thursday's growing continuing jobless claims - that it's taking a bit longer for laid off workers to find replacement gigs.

The average unemployment duration stretched to 22 weeks from 21.4, but that's a metric that seems to have found its equanimity, drifting sideways in the 19-22 week range for about two years now.

Viewed through the lens of race and ethnicity, the jobless picture looks increasingly bifurcated.

The White unemployment rate held steady at 3.5%, while joblessness increased for Hispanic, Asian and particularly Black workers.

Unemployment among Black Americans jumped 50 bps to 6.1%, widening the White/Black employment gap to 2.6 percentage points.

"Getting to full employment is particularly important for historically disadvantaged groups (e.g. young, noncollege, Black and Hispanic workers) who always experience a tougher labor market," blogs Elise Gould, senior economist at the Economic Policy Institute.

(Stephen Culp)

*****

Nvidia Propels Semiconductor Industry To $5.5 Trillion Valuation; Beginning Of Bigger Boom, Says Analyst

The U.S. semiconductor industry has hit a monumental milestone, amassing a combined market capitalization of $5.5 trillion as of Thursday. This achievement hypothetically positions the U.S. chipmaker industry as the world’s third-largest economy, surpassing Japan and trailing only behind the United States and China.

The industry’s spectacular growth stems from a surge in demand for artificial intelligence (AI) chips, propelling the overall market value to more than triple over the last year alone.

Leading this exponential growth, Nvidia Corp.NVDA commands more than half of the industry’s overall market value, amounting to approximately $3 trillion.

Nvidia’s share price has soared by 210% over the last year and 143% year-to-date, marking the strongest performance within the broader tech-heavy Nasdaq 100 Index. Reflecting its growth in the data center business, Nvidia’s revenue has risen at a compounded annual growth rate of 54% over the last three years.

Besides Nvidia, 10 other U.S. semiconductor companies boast market caps exceeding $100 billion, cementing the industry’s dominance. Six chipmakers also appear in the S&P 100, topping any other industry. Broadcom Inc.AVGO, with a market cap of $650 billion, ranks as the second-largest chipmaker and the eighth-largest U.S. company overall.

The 15 Biggest US Chipmakers By Market Capitalization

U.S. chipmaker exchanged traded funds (ETFs) are currently trading at record highs.

The VanEck Semiconductor ETF SMH and the iShares Semiconductor ETFSOXX have rallied 75% and 51%, respectively, over the past year. Nvidia’s larger weight in the SMH largely explains its higher performance compared to the SOXX ETF.

According to Bank of America equity analyst Vivek Arya, semiconductor stocks could face a pullback due to rising rates, the upcoming U.S. elections, geopolitical tensions, unfavorable AI headlines, and seasonal softness. Despite these potential headwinds, the investment bank remains bullish on chip stocks, particularly focusing on three favored themes:

Cloud (top picks: NVDA and AVGO)

Cars (top pick: NXP Semiconductor N.V.)

Complexity (top pick: KLA Corp.)

Understanding The Chip Cycle

Semiconductor cycles typically span around 3.5 years, with 10 up quarters followed by 4-5 down quarters, according to Arya.

The current upcycle began in late 2023, placing us in the third quarter, which suggests continued strength likely until mid-2026.

However, semiconductor stocks tend to change direction 6-9 months ahead of a cycle inflection, indicating that semis could potentially peak sometime around the second half of 2025, or roughly a year from now, the analyst explained.

“Many top tech and cloud companies are either lagging or still experimenting with training their large language models, where parameter sizes could increase by 10-100 times to reach multiple trillions of parameters,” Arya said.

Converting global data centers to accelerated computing could require $250-$500 billion annually, and we are only 20-30% into this transformation, which could last another 3-5 years.

The majority of the world’s food source is sustained via agriculture, making it a recession-resistant industry. Similar to most other industries, agriculture was also impacted during the COVID-19 pandemic. However, the group staged a recovery in the last two years as commodity prices soared on the back of easing of lockdown restrictions, higher global demand, and the Ukraine-Russia war, which squeezed supplies of key agricultural products, including wheat and fertilizers.

Several agriculture stocks are trading near record highs, even though prices for commodities such as wheat and corn have pulled back in the last year. On the other hand, fertilizer manufacturers are wrestling with a strong U.S. dollar DXY, making their products more expensive in emerging markets in Asia and Latin America.

Given the agriculture industry is quite large, investors can consider gaining diversified exposure by investing in exchange-traded funds (ETFs), which lowers equity-specific investment risk by a significant margin.

Here are three agriculture ETFs you can buy right now.

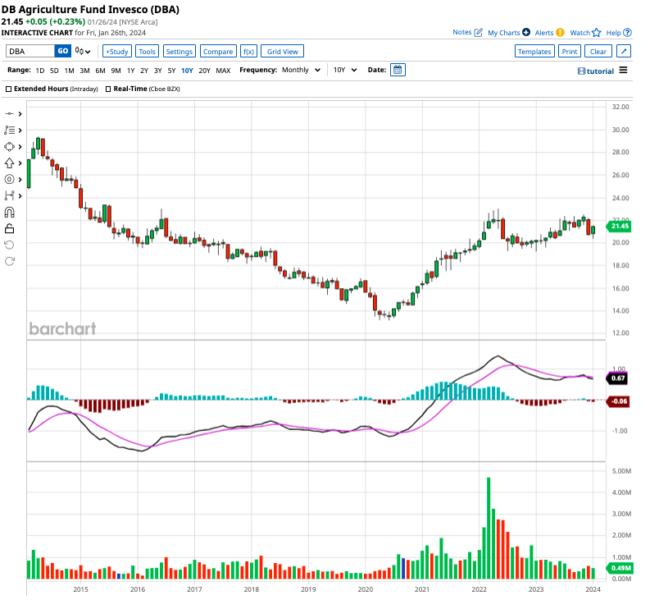

1. Invesco DB Agriculture Fund

The Invesco DB Agriculture Fund DBA is a popular option for those looking to gain exposure to agricultural commodities. The ETF invests in a basket of agricultural resources such as corn, soybeans, wheat, sugar, cocoa, coffee, cotton, and feeder cattle, offering investors diverse commodity exposure and a hedge against inflation.

Barchart

With $780 million in assets under management, the DBA ETF has an expense ratio of 0.91%, which is relatively high. Down 27% from all-time highs, DBA has gained 28% in the last three years.

The fund also pays shareholders an annual dividend of $0.96 per share, translating to a yield of 4.5%.

2. VanEck Agribusiness ETF

The VanEck Agribusiness ETF MOO offers exposure to a basket of equities involved in the agriculture business. Its top five holdings include Deere & Co. DE, Zoetis ZTS, Bayer BAYRY, Nutrien NTR, and Corteva CTVA, which account for 35.8% of the fund. While the majority of these holdings operate in developed markets, it also offers some exposure to emerging markets, such as Brazil and Malaysia.

The MOO ETF is positioned to benefit from the increase in global food demand and may offer a hedge against inflation, as agri-based commodities are generally the first to rise amid inflation.

With $927 million in assets under management, MOO has an expense ratio of 0.53%. This ETF trades 34% below all-time highs and has returned 68% in the past decade, after adjusting for dividends. MOO pays $2.24 in dividends annually for a forward yield of 3.1%.

3. iShares MSCI Agriculture Producers ETF

The final ETF on my list is the iShares MSCI Agriculture Producers ETF VEGI, which provides exposure to agricultural commodity prices via a portfolio of equities in the agri-business segment. These holdings include companies such as Deere & Co., Corteva, Archer-Daniels-Midland ADM, Nutrien, and Lamb Weston LW, which together account for 45% of the ETF's weight.

With $149 million in assets under management and an expense ratio of 0.39%, the VEGI ETF is the cheapest ETF on this list.

Down 25% from all-time highs, VEGI shares have gained 70% in dividend-adjusted gains since January 2014. The ETF pays shareholders an annual dividend of $0.55 per share, indicating a forward yield of almost 2.7%.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

BUZZ - Nasdaq top and bottom performing stocks at about 12:01 p.m. EDT

The Nasdaq 100 NDX lost 40.50 points, or 0.22%, to 18,214.19 and recorded 6 new highs and no new lows. 29 stocks rose and 72 fell as declining issues outnumbered advancers by about a 2.5-to-1 ratio.

Buy a Krispy Kreme at McDonald's. It's the New Super Breakfast Deal. — Barrons.com

Krispy Kreme's deal to sell its popular doughnuts at McDonald's restaurants across the U.S. is a win for both companies: Krispy Kreme expands its reach while McDonald's expands its menu at a low cost to attract more customers.

The partnership, announced Tuesday, comes as consumers are looking for cheaper options amid higher food prices. Breakfast remains a key battleground among fast-food chains. Wendy's recently said it plans to invest $55 million in advertising its breakfast options, and it estimates a 50% increase in weekly U.S. breakfast sales over the next two years.

Krispy Kreme shares jumped 39% on news of the deal Tuesday. The stock gave back some of the gains on Wednesday, closing 11.5% lower to $15.35. McDonald's was up 1.2%.

Krispy Kreme sells doughnuts through its nearly 400 independent shops as well as thousands of grocery stores and quick-service restaurants. The company bakes doughnuts daily at production hubs and delivers to nearby retailers.

The Charlotte, N.C.-based company has been working to expand its distribution network and drive up sales per hub. In 2023 alone, the firm placed its products in 2,300 new locations, growing the total to about 14,000 globally, about half of which in the U.S.

Krispy Kreme has supplied doughnuts at 160 McDonald's restaurants in Kentucky since 2022 as a test concept. The expanded partnership gives it access to the majority of McDonald's nearly 14,000 restaurants, almost doubling its U.S. distribution. The doughnuts will be sold throughout the day.

"Krispy Kreme is not a packaged food company. The whole brand promise is that it's fresh," said Andrew Wolf, an analyst at investment bank C.L. King & Associates. "When you're in the fresh business, it's very local, and this partnership will give them a lot of local market share."

The move will help the company grow its economies of scale and significantly drive down the incremental costs of logistics and infrastructure, says Wolf: "The closer the units are to each other, the cheaper it is to deliver."

McDonald's foot traffic at its U.S. locations is strong, according to location intelligence firm Placer.ai, as more mid-income consumers trade down from full-service restaurants to fast-food chains.

McDonald's accounts for more than a third of total visits to fast-food restaurants and coffee and bakeries shops in the mornings, far surpassing Starbucks and Dunkin', which account for about 15% each of the traffic, according to Placer.ai.

The addition of Krispy Kreme doughnuts to the menu could help the fast-food giant expand sales and enhance its dominance among peers, especially during breakfast hours.

The partnership is "a way to recapture some of Covid's lapsed breakfast users with a differentiated product and limited incremental labor costs, " analysts from Evercore wrote in a note.

The partnership will start rolling out in the second half of this year, and across the U.S. by the end of 2026. Krispy Kreme won't supply other quick-service restaurants in the U.S. during the period.

"This is clearly a strong development for Krispy Kreme, increasing the availability and number of occasions consumers can try a Krispy Kreme doughnut," Truist analyst Bill Chappell wrote in a note.

The next challenge for Krispy Kreme is to ramp up production to meet the new demand. CEO Josh Charlesworth said last month that the firm has started investing in new doughnut-making sites to prepare for the rollout.

The firm's current production hubs could serve about 6,000 McDonald's restaurants with modest incremental capital spending, Wolf said. To meet the increased demand, Krispy Kreme would need to add 25 to 30 more production hubs.

Wolf expects Krispy Kreme's capital expenditures in 2024 to total between $120 million and $140 million, or 7% to 8% of its revenue, which could increase in 2025 and 2026.

The company could add $375 million to $400 million in incremental sales by the end of 2027, with a growth of 35 cents to 40 cents earnings per share, he estimates. Krispy Kreme posted an EPS of 27 cents in 2023. Wolf raised his 2025 EPS outlook to 55 cents from a prior 45 cents, and lifted his price target for the stock to $22 from $18.

Sales at Krispy Kreme have been growing around 10% annually over the past two years. Yet the stock has been choppy since it was listed in 2021. Concerns over inflation-driven softer demand and weight-loss drugs like Ozempic and Mounjaro have hurt the stock.

Investors should play the long game. Earnings will likely decline before stepping back up as start-up costs offset additional profit, wrote Truist's Chappell. The option of buying Krispy Kreme at McDonald's could also hurt sales at nearby grocery stores that also sell the doughnuts.

Write to Evie Liu at evie.liu@barrons.com

This content was created by Barron's, which is operated by Dow Jones & Co. Barron's is published independently from Dow Jones Newswires and The Wall Street Journal.

Bulls Stampede On Fed's Dovish Signal, Nasdaq 100 Hits New Record High, DOJ Sues Apple: What's Driving Markets Thursday?

Bulls are on fire in the aftermath of the Federal Reserve’s March policy meeting, igniting a rally in stocks across the board on Wall Street.

The S&P 500 index surged above 5,250 points, continuing its upward trajectory to set new record highs. All eleven sectors of the S&P 500 posted gains.

Meanwhile, the tech-heavy Nasdaq 100 surpassed 18,440 points, also achieving unprecedented all-time highs. The Dow Jones added over 300 points, edging closer to the historic milestone of 40,000 points.

In a notable display of risk sentiment, small caps also rose as evidenced by the iShares Russell 2000 ETF IWM up by 0.9%.

Shares of Apple Inc.AAPL faced a setback, down over 3%, as the Justice Department and 16 state attorneys general filed an antitrust lawsuit against the tech giant. The lawsuit alleges that Apple exerted monopolistic control in the smartphone market.

The U.S. dollar index rose, driven by significant gains of the greenback against the British pound and the Swiss franc, the latter of which suffered due to an unforeseen rate cut by the Swiss National Bank.

Gold paused for a breather, down 0.5%, after closing above $2,200 on Wednesday. Bitcoin fell 2% to $66,400.

Thursday’s Performance In Major US Indices, ETFs

Major Indices

Price

1-day %chg

Nasdaq 100

18,447.55

1.1%

Russell 2000

2,099.85

0.8%

Dow Jones

39,837.39

0.8%

S&P 500

5,261.46

0.7%

The SPDR S&P 500 ETF TrustSPY rose 0.7% $523.87, the SPDR Dow Jones Industrial AverageDIA rose 0.8% to $398.19 and the tech-heavy Invesco QQQ TrustQQQ rallied 1.2% to $449.06, according to Benzinga Pro data.

Among sectors, the IndustrialsSelect Sector SPDR FundXLI was the top performer for the day, up 1.1%, while the Utilities Select Sector SPDR FundXLU was the laggard with a flat performance.

Thursday’s Stock Movers

Shares of Reddit Inc.RDDT are indicated to open at $50-$52, in their first day of trading.

Micron Technology, Inc. MU rallied nearly 16% following the memory chipmaker’s earnings announcement.

Chipmaker peers such as Broadcom Inc.AVGO rose 9% following a bullish note from Goldman Sachs.

Other stocks moving on earnings are Steelcase Inc.SCS (down over 10%) and Five Below, Inc. FIVE (down about 15%), Accenture plc ACN (down 8%), Winnebago Industries, Inc. WGO (up over 5%) and Shoe Carnival, Inc. SCVL (up nearly 7%), Darden Restaurants, Inc. DRI (down 6%).

Those reporting after the close include FedEx Corporation FDX, Lululemon Athletica Inc. LULU, NIKE, Inc.NKE and Worthington Steel, Inc. WWS.

Wall Street exhaled a sigh of relief as the Federal Reserve’s favored gauge of inflation cooled as anticipated in January, quelling fears that an unexpected rise in the Consumer Price Index (CPI) might spill over into the Personal Consumption Expenditure (PCE) price index.

At noon in New York, the Nasdaq 100 was up 0.4%, striving to erase losses from Wednesday. The S&P 500 Index and the Dow Jones Industrial Average exhibited more subdued reactions, with gains of 0.1% and a decline of 0.2%, respectively, while the Russell 2000 edged 0.3% higher.

Among major tech stocks, Advanced Micro Devices Inc.AMD stands out, surging over 6% to achieve a new all-time high, emerging as the top performer in the semiconductor sector today.

Conversely, Apple Inc.AAPL continues to deliver lackluster results, dropping 1% to $178, marking its tenth negative day out of the last thirteen and poised to close at its lowest levels since early November 2023. Recent reports indicate that Apple’s iPhone 15 series is being heavily discounted by resellers in China, signaling a sustained decline in demand.

Treasury yields edged lower as traders adjust their positions in anticipation of a rate cut in June. The popular iShares 20+ Year Treasury Bond ETFTLT rose 0.6%.

In the volatile crypto market, Bitcoin is down over 2% to $61,000, after hitting an intraday high of $63,675.

Thursday’s Performance In Major Indices, ETFs

Major Indices

Price

1-day % Chg

Nasdaq 100

17,949.36

0.4%

Russell 2000

203.07

0.4%

S&P 500

5,077.32

0.1%

Dow Jones

38,881.01

-0.2%

The SPDR S&P 500 ETF TrustSPY was 0.1% higher to $506.76, the SPDR Dow Jones Industrial AverageDIA fell 0.1% to $389.15 and the tech-heavy Invesco QQQ TrustQQQ rose 0.4% to $437.06, according to Benzinga Pro data.

The Real EstateSelect Sector SPDR FundXLU, was the notable outperformer for the second straight session, up by 0.8%, while the Health Care Select Sector SPDR FundXLE continued to lag behind, down 0.6%.

Thursday’s Stock Movers

Crypto-related stocks took a hit as Bitcoin prices fell. Marathon Digital Holdings Inc.MARA tumbled over 17%, despite the company reported sharply higher-than-predicted profits last quarter. Peers Riot Platforms Inc. RIOT, Bit Digital Inc.BTBT and Coinbase Global Inc. COIN fell 12%, 6.5% and 2.5%, respectively.

Snowflake Inc.SNOW tumbled nearly 20%, after the company announced that CEO Frank Slootman has decided to retire from his role as CEO. The AI-related company saw its revenue and earnings beating Wall Street’s analyst predictions last quarter.

Hormel Foods Corp. HRL rose over 13%, marking the highest daily performance among S&P 500 stocks, after the company unveiled better-than-expected results last quarter.

Other companies reacting to earnings were Monster Beverage Corp.MNST, up 5.7%, Celsius Holdings Inc.CELH, up 19%, Okta Inc.OKTA, up 19%, Hayward HoldingsInc.HAYW, up 15%, Natera Inc.NTRA, up 12%, The Chemours CompanyCC, down 31%, DoubleVerify Holdings Inc. DV, down 17%, AMC Entertainment Holdings Inc.AMC.

Stocks reporting after the close include Autodesk, Inc.ADSK, Cooper Companies, Inc. CCOO, Fisker, Inc. FSR, Zscaler, Inc. ZS, Hewlett Packard Enterprises Company HPE, NetApp, Inc. NTAP and SoundHound AI, Inc. (NASDAQ:SOUND).

Now Read:Argentine Stocks Rebound As President Milei Eyes Potential New IMF Deal, Exit From Capital Controls

C3.ai shares AI jumped 24% to a six-month high on Thursday after the AI software firm delivered third-quarter results ahead of Wall Street expectations and narrowed its full-year revenue forecast on strong enterprise demand.

The company's shares have gained 227% since the end of 2022, valuing it at $4.46 billion, as it draws strong interest from retail investors looking to bet on the boom in artificial intelligence (AI).

However, Nvidia NVDA, the poster child for AI, has rocketed 445% in market value during the same period.

Strong demand from federal customers helped C3.ai's subscription revenue increase 23% in the reported quarter to $70.4 million and beat estimate of $66.77 million, according to LSEG data. Subscriptions generate about 90% of total revenue.

"The company is having notable success in the federal sector while signing more multi-year subscription agreements that trend similarly to consumption revenue behavior," said D.A. Davidson analyst Gil Luria.

Other AI-related stocks including BigBear.ai Holdings BBAI, Guardforce AI GFAI, Arm Holdings ARM and Nvidia NVDA gained between 2.5% and 10%, with SoundHound AI SOUN climbing 9% ahead of its fourth-quarter results due after markets close.

C3.ai's stock was last trading at $37, above the $30 median price target of the 14 brokerages covering C3.ai. Their average rating, according to LSEG data, is "hold".

Shares of the software company were among the top trending tickers on retail trader forum Stocktwits.

Redwood City, California-based C3.ai also narrowed its 2024 revenue forecast to $306-$310 million, from $295-$320 million.

Still, the new forecast was largely above analysts' estimates of $306.1 million.

The company also said Chief Accounting Officer Hitesh Lath will transition to the chief financial officer role, effective March 1, replacing Juho Parkkinen.

Parkkinen will remain as vice president of finance, C3.ai said.

BUZZ - Nasdaq top and bottom performing stocks at about 12:01 p.m. EST

The Nasdaq 100 NDX gained 19.89 points, or 0.11%, to 17,953.22 and recorded 8 new highs and no new lows. 53 stocks rose and 48 fell as advancing issues outnumbered decliners by a about a 1.1-to-1 ratio.

Eikon search string for individual stock moves:STXBZ

Wall Street's main indexes were subdued on Friday after a hotter-than-expected producer prices report pushed back market speculations of imminent interest rate cuts by the U.S. Federal Reserve.

At 13:46 ET, the Dow Jones Industrial Average DJI was down 0.01% at 38,771.14. The S&P 500 SPX was up 0.03% at 5,031.2 and the Nasdaq Composite IXIC was down 0.21% at 15,872.013.

The top three S&P 500 (.PG.INX) percentage gainers:

** Bio-Rad Laboratories Inc , up 8.6%

** Applied Materials Inc , up 8.1%

** Vulcan Materials Co , up 6.3%

The top three S&P 500 (.PL.INX) percentage losers:

The Nasdaq 100 NDX lost 33.69 points, or 0.19%, to 17,773.94 and recorded 11 new highs and 2 new lows. 59 stocks rose and 41 fell as advancing issues outnumbered decliners by a about a 1.4-to-1 ratio.

For all the attention paid to the highflying tech giants dubbed the Magnificent Seven, there's another grouping that has kept right up with them, and with a lot lower risk.

It's called GRANOLAS, a term coined by Goldman Sachs during 2020 to refer to the largest European companies at that time: GSK (GSK), Roche (CH:ROG), ASML (ASML), Nestle (CH:NESN), Novartis (CH:NOVN), Novo Nordisk (NVO), L'Oreal (FR:OR), LVMH (FR:MC), AstraZeneca (AZN), SAP (SAP) and Sanofi (SNY).

This chart shows, in total return terms since January 2021, that the GRANOLAS grouping has kept right up with the Magnificent Seven of Amazon.com (AMZN), Apple (AAPL), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA) and Tesla (TSLA), with a 63% return, and volatility since 2018 that is on average twice was low.

They're a lot cheaper than the Mag 7, trading at 20 times earnings versus 30, though the GRANOLAS are more expensive to the broader European market.

This grouping has had a strong fourth quarter reporting season, led by Novo Nordisk's success with weight-loss drugs, and ASML's surge of orders for microchip-equipment making machines, although L'Oreal disappointed in part due to its struggles in China.

"In our view, the reason why this group of stocks trades at a premium to the market is that they offer strong (and predictable) growth," said strategists led by Guillaume Jaisson.

They say the time to own the GRANOLAS is when global GDP growth is below 3%, which is what the bank expects over the next five years.

Perhaps surprisingly in a world stuffed with exchange-traded funds, Goldman has not created a fund to trade on its moniker, meaning investors who want exposure to the theme would have to buy each stock individually.

-Steve Goldstein

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.

Nervous About Nvidia, Tesla and the Magnificent 7? Look at Goldman's GRANOLAS. — Barrons.com

The Magnificent 7 tech stocks have been the driving force behind the S&P 500's rally to record highs. For investors feeling nervous about this top-heavy market dynamic, there's a new group that may warrant a look: the GRANOLAS.

Coined by Goldman Sachs, the GRANOLAS represent some of the largest European companies by market capitalization: GSK, Roche, ASML, Nestlé, Novartis, Novo Nordisk, L'Oréal, LVMH, AstraZeneca, SAP, and Sanofi. Their collective performance has been astonishing over the past few years, even if it hasn't been nearly as eye-catching as the Magnificent 7, which includes Microsoft, Apple, Alphabet, Amazon.com, Nvidia, Tesla, and Meta Platforms.

The GRANOLAS accounted for 60% of all gains over the past year in Europe, where the stocks make up a quarter of the market capitalization of the pan-European Stoxx 600 index, Goldman Sachs analyst Guillaume Jaisson wrote in a Monday note. The 11 stocks are a key reason why European equities have performed well despite lagging economic growth in the region, Jaisson added.

"From a global point of view, the GRANOLAS have even outperformed the so-called Magnificent 7 over the past two years," Jaisson wrote. "Their (out)performance is even more impressive on a risk-adjusted basis: with a volatility 2x lower than for the Magnificent 7."

Indeed, the GRANOLAS have delivered better returns for less risk than the Magnificent 7, according to Goldman Sachs — and that's not their only quality. While the group trades at a premium 20 times price-to-earnings ratio, it's a 30% discount to the Magnificent 7 — at 30 times — and below their historical discount. The GRANOLAS also offer an average dividend yield of 2.5%, which is much higher than the S&P 500's average 1.5% and the meager 0.3% dividend offered by the Magnificent 7.

"The GRANOLAS exhibit qualities that we expect to predominate in this cycle: strong earnings growth, low volatility, high & stable margins, and strong balance sheets," wrote Jaisson. "We think they also stand to benefit from the structural shift towards passive investment and the lack of liquidity in the European equity market."

The GRANOLAS moniker sounds like more of a cereal category than a stock strategy, but if Goldman Sachs is right then these names might be worth a look for a balanced portfolio.

Write to Jack Denton at jack.denton@barrons.com

This content was created by Barron's, which is operated by Dow Jones & Co. Barron's is published independently from Dow Jones Newswires and The Wall Street Journal.

BUZZ - Nasdaq top and bottom performing stocks at about 03:45 p.m. EST

The Nasdaq 100 NDX gained 174.80 points, or 0.98%, to 17,957.97 and recorded 19 new highs and 2 new lows. 67 stocks rose and 34 fell as advancing issues outnumbered decliners by a about a 2-to-1 ratio.

Pharmacy Chains Are in a World of Hurt. Blame Shrinking Drug Reimbursements. — Barrons.com

In eight years, national pharmacy chains have gone from an invasive species to an endangered one.

They arrived in the 1980s like a beetle to a hardwood forest, burrowing into virtually every suburban strip mall, rural township, and urban business district in the U.S. By 1990, there were 18,600 chain pharmacies across the country; by 2010, there were more than 22,500.

The chains had some great years. They squeezed out independent pharmacies, a third of which closed between 1990 and 2010. The share prices of the two biggest chains, now known as Walgreens Boots Alliance and CVS Health, multiplied around 14 times between the start of 1995 and the middle of 2015, while the S&P 500 index only quadrupled. Walgreens'

total revenue climbed from $42.2 billion in 2005 to $103.4 billion in 2015, while CVS' revenue grew from $37 billion to $153.3 billion over the same period.

Today, their entire business model is under pressure. You can see it in the October bankruptcy filing of Rite Aid, the third-largest of the U.S. chains; in the share price of CVS, which is down more than 30% over the past two years; in the unrest among chain pharmacists, who have held sporadic walkouts in some cities.

Turning the chains around won't be easy. Their biggest problem has been the declining reimbursement rates that pharmacy-benefit managers pay them for the prescription drugs they sell, says John Ransom, an analyst who covers Walgreens for Raymond James. Those cost pressures are unlikely to disappear.

Adjusted operating income for Walgreens' U.S. retail pharmacy division, which encompasses the retail stores and the pharmacy counters they contain, fell from $5.4 billion in the company's 2016 fiscal year to $3.7 billion in the company's 2023 fiscal year, which ended in August, a 31.1% drop. At CVS, the company's retail pharmacy division, which also includes its long-term care pharmacies, had operating profits of $7.3 billion in 2016. It has since changed how it reports results; its new retail pharmacy division had adjusted operating income of $6 billion in 2023. As profits have dropped, the chains have begun closing hundreds of stores.

Among the 20 analysts tracked by FactSet who cover Walgreens, only three rate it a Buy or Overweight, even though the stock trades at less than seven times earnings expected over the next 12 months. Most rate the stock a Hold, an indication of the work the company needs to do to rebuild investor confidence.

As for CVS, the company's prospects are less dependent on its retail outlets, and its share price, at a recent $75.08. is more closely tied to the performance of Aetna, its insurer. Three-quarters of analysts tracked by FactSet rate it Buy or Overweight; their average target price is $89.47.

The chain retail pharmacies remain an important part of the U.S. healthcare system, supplying everything from antibiotics to blood pressure monitors and vaccines to hundreds of millions of Americans. Fixing them will take reconsideration of the purpose of a chain drugstore. Both CVS and Walgreens are expanding the healthcare services they provide, as they seek new justifications for their immense nationwide footprint. That shift will take years, and the prospects for these new strategies are uncertain: Walgreens is closing dozens of clinics in its primary-care chain amid profitability troubles.

Over the past few months, something has shifted at the big pharmacy chains. Both CVS and Walgreens have signaled an openness to big, structural changes in how they operate their businesses. The new approaches at the pharmacy counter, and store closings, could stanch the bleeding at the big retail pharmacy chains.

But these changes, particularly the store closings, could create real challenges for people who rely on those stores for their prescriptions.

"The reality is that we need all kinds of pharmacies in order to be able to provide the level of access to care and pharmacy services that our society needs in the U.S., but we've got to have a model that supports that," says Michael Hogue, CEO of the American Pharmacists Association, which backed some of this fall's walkouts, where pharmacists refused to show up to work at retail chains to draw attention to their concerns about understaffing. "We just have not had a model that's been supportive."

The companies are already shuttering some stores, generally citing population shifts and changes in buying patterns. CVS said in late 2021 it plans to close 900 locations through the end of this year, and Walgreens is in the process of closing up to 500 U.S. stores. Rite Aid's future plans are obscured by the bankruptcy proceedings, but The Wall Street Journal reported last year that the company has proposed closing as many as 500 of its stores, and has announced definitive plans to close almost 200 in the months since it filed for bankruptcy protection.

In a statement to Barron's, Rite Aid said it had closed certain stores to reduce its spending on rent and strengthen its financial position. "At this time, we have not made or confirmed any decisions on additional specific store closures as part of our financial restructuring process," the company said.

Charles Rhyee, who covers Walgreens and CVS for TD Cowen, says that the chain pharmacies should consider closing far more stores than they have proposed , while keeping open those that fit in with their efforts to expand into healthcare services. "I think they're slowly getting there, but maybe from an investor standpoint you would want something a little faster," he says. He acknowledged that store closings are made difficult by long leases.

Walgreens CEO Tim Wentworth, who took over leadership of the company late in 2023, says that dramatic waves of store closings aren't in the works, and that having a big national footprint is important as the company increases the healthcare services it offers. "I don't believe we have too few stores," he says. "I believe there is room to move our footprint probably modestly downward. But that by itself is not as big a leverage as making sure that we've got really good points of distribution for patients."

CVS, for its part, says that it will "continue to take a thoughtful approach in evaluating the size of our retail footprint," but that it plans to maintain "a national presence that provides convenient access to pharmacy services, including in underserved communities."

A big chunk of the problem facing the chain pharmacies is that people don't shop like they did in the 1990s. During their period of rapid expansion, online shopping was in its infancy, and if you wanted batteries and a toothbrush, a quick 10 p.m. trip to CVS was the ultimate in convenience. The companies put their stores at the "corner of Main and Main," as Walgreens' CEO at the time liked to say, and would boast about the proportion of the U.S. population that lived within five miles of one of their locations. Today, that number is around 85% for CVS and 78% for Walgreens.

Shopping habits since then have changed, and multiple national retail chains have declared bankruptcy.

While concerns about shoplifting have led chain pharmacies to lock up items at certain locations, the impact of shoplifting on the profitability of the individual companies is hard to measure. Neither CVS nor Walgreens break out their shoplifting losses in financial reports, though Walgreens cited "higher shrink levels" as one reason behind a drop in its gross margins in its quarter ended in November 2023. At an investor conference in January, Wentworth said that the impact of shoplifting is different from store to store, and that the company assumes that shoplifting levels won't drop in the near-term.

For the retail pharmacy chains, shoplifting and shifts in retail consumer habits aren't their biggest problem. That's because Americans still prefer to pick up their medicines in person. So-called front-of-store offerings, like candy and batteries, account for just a quarter of sales at Walgreens and CVS.

Most of the revenue comes from the pharmacy counter, where consumer habits haven't changed all that much. In 2022, mail-order pharmacies filled just 9% of U.S. prescriptions, compared with 47% filled by chain pharmacies, according to the Drug Channels Institute. That's roughly the same as the breakdown in 2010, when mail-order pharmacies filled 7% of prescriptions and chain pharmacies filled 48%, according to a 2012 report from the National Association of Chain Drug Stores.

That means that the troubles facing the retail pharmacies lie not so much in the broader shift to online shopping but in what goes on behind the pharmacy counter itself.

Pharmacies buy their prescription drugs from a distributor like Cardinal Health, then get reimbursed by pharmacy-benefit managers, which contract with the patients' insurer. The terms of those reimbursements are complex, and retail pharmacy executives have complained for years that they allow less and less room for profit.

The problem is that the chain pharmacies have little leverage in their negotiations with the pharmacy-benefit managers, which have accrued enormous power in the drug chain. Three large PBMs, including CVS-owned Caremark, process 80% of U.S. prescriptions, according to the Drug Channels Institute. (CVS says that its pharmacy negotiates with Caremark just as it negotiates with other PBMs, and that there are "strict firewalls" between CVS Pharmacy and Caremark.) The pharmacies need to cut deals with those PBMs in order to access patients. Meanwhile, the chain pharmacies face enormous competition on the pharmacy side, much of it from retailers whose business models rely much less on profits made at the pharmacy counter. Of the roughly 58,900 pharmacy counters in the U.S. in 2022, 16,800 were located inside of supermarkets or mass-market merchants like Walmart, according to the Drug Channels Institute.

That dynamic has pushed the reimbursement rates lower and lower. "The question is, why do they keep taking these lower and lower reimbursement rates?" says Ransom, the Raymond James analyst. "And the answer is that while the contracts are still profitable, the PBMs are going to push this right to the line every time."

A spokesperson for the Pharmaceutical Care Management Association, a trade organization representing PBMs, said that the PBMs are simply responding to high drug prices. "Blaming PBMs misses the fundamental reason for high-cost drugs, which is the prices set by drug companies," said PCMA spokesman Greg Lopes. "The job of the PBM is to keep the cost of prescription drugs as low as possible for employers and their employees, and we do that."

Ransom says that chain pharmacies could ease some of their financial pressures by shrinking. "We think drugstore counters need to significantly contract," he wrote in an October note to investors. Thanks to long leases, the number of chain drugstores locations has barely budged. Despite all the changes in consumer habits and in the pharmacy business, the number of chain drugstores in 2022 was 20,900, down only slightly from the 22,600 in 2010.

Fewer pharmacies would give each one more power to negotiate with the PBMs.

"What would make this work is [if] they get pricing power," Ransom says. "What would give them pricing power? Scarcity."

On top of the lower reimbursement rates, the growing role of cheap generics has taken another bite out of pharmacy counter profits. Since the reimbursements the pharmacies receive from the PBMs are tied to the cost of the drugs they process, more cheap drugs means lower revenue. In 2018, 90% of prescriptions in the U.S. were for generics, up from 75% in 2009, according to the Congressional Budget Office. The prices of generic drugs, meanwhile, have been falling since 2010.

Walgreens' Wentworth, who previously ran Cigna's pharmacy benefit manager, says that the relationship between the PBMs and the pharmacies isn't working. "It's becoming distorted to where the retailers need to, frankly, reset the conversations with PBMs," he says.

CVS in early December proposed its own solution, announcing a new proposed model for how its pharmacies will get paid by the PBMs. The new model will be simpler and more transparent, the company said, and will tie the pharmacy's level of reimbursement directly to the cost of the drug plus a set markup and a per-patient fee. Executives said in an investor presentation that the new model would "reset the financial outlook" for the retail business.

"It ensures the sustainability of retail economics," CVS Chief Pharmacy Officer Prem Shah said on a Dec. 5 investor day presentation.

The company still needs to convince PBMs to play ball. In response to a question from Barron's, a CVS spokesperson said that the company plans to implement the new model starting in 2025, and that feedback had been "positive." There are indications that the PBMs are thinking along the same lines, which could bode well for adoption. Earlier in 2023, Optum Rx, the UnitedHealth Group-owned PBM, introduced its own set of new payment models, constructed along similar lines as the CVS proposal.

On an investor call in February, CVS CEO Karen Lynch said that the company was "actively engaged in constructive discussions" with several PBMs about the new model.

The CVS plan is an ambitious one, and reflects pressure on companies up and down the drug supply chain from efforts like the Mark Cuban Cost Plus Drugs Company, which sells generic drugs using a similar pricing model.

Wentworth said that Walgreens, too, would like to shift to similar cost-plus contracting models. "If they want them, we are more than willing to do it," he said of the PBMs.

The CEO is clear-eyed about the challenges facing Walgreens. But for the first time in years, there is a clear path to resetting the retail pharmacy chain business. The companies must proceed carefully as they consider closing more stores, but fewer chain pharmacies seems inevitable over the next few years. For investors, a trend toward a smaller number of chain pharmacies, and a resetting of the relationships with the PBMs, could slowly ease the pressures on the model, as the companies work toward reinvention.

Wentworth said there could be an industrywide shift toward simplified contracts, amid pressure from payers and regulators. "There feels like there's some pull here," he says. "It may come to pass. It's not going to be overnight."

Write to Josh Nathan-Kazis at josh.nathan-kazis@barrons.com

This content was created by Barron's, which is operated by Dow Jones & Co. Barron's is published independently from Dow Jones Newswires and The Wall Street Journal.

Equity Markets Mixed late Tuesday as Traders Weigh Fed Official Comments, Corporate Earnings

US benchmark equity indexes were struggling for direction ahead of Tuesday's close as markets evaluated the latest remarks by a Federal Reserve official, along with corporate financial results.

The Dow Jones Industrial Average was up 0.1% at 38,428, while the Nasdaq Composite fell 0.2% to 15,564.8. The S&P 500 was little changed at 4,942.9. Among sectors, materials and real estate paced the gainers. Technology and communication services were in the red.

Cleveland Fed President Loretta Mester said it would be "a mistake" to lower interest rates too soon or too quickly without enough evidence that inflation was on a sustainable and timely path back to the Federal Open Market Committee's 2% target.

Eli Lilly LLY, Fiserv FI, Carrier Global CARR, Spotify Technology SPOT, and GE HealthCare Technologies GEHC were among the companies that reported their latest financial results Tuesday.

Amgen AMGN, Chipotle Mexican Grill CMG, Ford Motor F and Snap SNAP are among the companies scheduled to report after the closing bell.

The US 10-year yield slid 8.3 basis points to 4.08%, while the two-year rate retreated 7.3 basis points to 4.4%.

West Texas Intermediate crude oil rose 0.9% to $73.46 per barrel.

BUZZ - S&P 500 top and bottom performing stocks at about 12:00 p.m. EST

Eikon search string for individual stock moves:STXBZ

U.S. stocks surged on Friday, with the benchmark S&P 500 scaling a fresh record, as investors cheered robust quarterly reports from Meta Platforms and Amazon.com, while a strong jobs report kept the upbeat sentiment in check.

At 13:31 ET, the Dow Jones Industrial Average DJI was up 0.20% at 38,597.82. The S&P 500 SPX was up 0.94% at 4,952.22 and the Nasdaq Composite IXIC was up 1.52% at 15,595.63.

The top three S&P 500 (.PG.INX) percentage gainers:

Eikon search string for individual stock moves:STXBZ

The benchmark S&P 500 was subdued on Tuesday as investors assessed earnings reports from legacy companies United Parcel Service and General Motors, as well as data that signaled a mixed labor market.

At 13:34 ET, the Dow Jones Industrial Average DJI was up 0.26% at 38,434.83. The S&P 500 SPX was down 0.07% at 4,924.35 and the Nasdaq Composite IXIC was down 0.69% at 15,520.792.

PFE, one of the world’s largest pharmaceutical firms, is on the verge of a bullish Golden Cross, a significant technical indicator suggesting potential upward momentum for the stock.

PFE, one of the world’s largest pharmaceutical firms, is on the verge of a bullish Golden Cross, a significant technical indicator suggesting potential upward momentum for the stock.

JPM, Bank of America

JPM, Bank of America  BAC, Wells Fargo

BAC, Wells Fargo  WFC, Discover Financial

WFC, Discover Financial  DFS, KeyCorp

DFS, KeyCorp  KEY and Synchrony Financial

KEY and Synchrony Financial  SYF, are seen as some of the likely winners by the brokerage.

SYF, are seen as some of the likely winners by the brokerage. COIN, Marathon Digital

COIN, Marathon Digital  MARA and Riot Platforms

MARA and Riot Platforms  RIOT, have surged tracking gains in bitcoin after a failed assassination attempt on the former president raised his odds of winning the elections in November.

RIOT, have surged tracking gains in bitcoin after a failed assassination attempt on the former president raised his odds of winning the elections in November. FSLR, NextEra Energy

FSLR, NextEra Energy  NEE and Sunrun

NEE and Sunrun  RUN to stay if Biden is re-elected.

RUN to stay if Biden is re-elected. ETN, Quanta Services

ETN, Quanta Services  PWR, Tesla

PWR, Tesla  TSLA and Air Products and Chemicals

TSLA and Air Products and Chemicals  APD, according to UBS.

APD, according to UBS. JCI and Trane Technologies

JCI and Trane Technologies  TT, as well as waste management companies with recycling infrastructure such as Waste Management

TT, as well as waste management companies with recycling infrastructure such as Waste Management  WM and Republic Services

WM and Republic Services  RSG.

RSG. XOM, Cheniere Energy

XOM, Cheniere Energy  LNG and ConocoPhillips

LNG and ConocoPhillips  COP under Trump 2.0.

COP under Trump 2.0. F and General Motors

F and General Motors  GM and steel producers such as Nucor

GM and steel producers such as Nucor  NUE and Steel Dynamics

NUE and Steel Dynamics  STLD, UBS analysts say.

STLD, UBS analysts say. DJT, in which the former president owns a majority stake, software firm Phunware

DJT, in which the former president owns a majority stake, software firm Phunware  PHUN and video-sharing platform Rumble

PHUN and video-sharing platform Rumble  RUM.

RUM. GEO and CoreCivic

GEO and CoreCivic  CXW may benefit from Trump's re-election, on promises of a crackdown on illegal immigration and restrictions on legal immigration, which could boost demand for detention centers.

CXW may benefit from Trump's re-election, on promises of a crackdown on illegal immigration and restrictions on legal immigration, which could boost demand for detention centers. LLY and Merck

LLY and Merck  MRK, as well as health insurers such as Humana

MRK, as well as health insurers such as Humana  HUM and UnitedHealth

HUM and UnitedHealth  UNH.

UNH. GS, Morgan Stanley

GS, Morgan Stanley  MS, Lazard LLAZ and Evercore

MS, Lazard LLAZ and Evercore  EVR, which benefit from M&A activities, to gain from such a policy change.

EVR, which benefit from M&A activities, to gain from such a policy change. AMAT, KLA Corp

AMAT, KLA Corp  KLAC, Intel

KLAC, Intel  INTC and Texas Instruments

INTC and Texas Instruments  TXN.

TXN. DE and Tractor Supply Company

DE and Tractor Supply Company  TSCO, UBS analysts say.

TSCO, UBS analysts say. COPX up 1.6%

COPX up 1.6% IWM up 1%

IWM up 1% KRE up 0.9%

KRE up 0.9% XLE up 0.9%

XLE up 0.9% GDX up 0.7%

GDX up 0.7% DJI was down 0.06% at 38,775.82. The S&P 500

DJI was down 0.06% at 38,775.82. The S&P 500  SPX was up 0.13% at 5,353.7 and the Nasdaq Composite

SPX was up 0.13% at 5,353.7 and the Nasdaq Composite  IXIC was up 0.28% at 17,181.094.

IXIC was up 0.28% at 17,181.094. WMT: up 1.3%

WMT: up 1.3% CRWD: up 9.2%

CRWD: up 9.2% GDDY: up 2.4%

GDDY: up 2.4% GME: down 14.4%

GME: down 14.4% OXY: up 1.9%

OXY: up 1.9% PLNT: up 3.9%

PLNT: up 3.9% LUV: up 8.4%

LUV: up 8.4% NVDA: up 0.9%

NVDA: up 0.9% DO: up 10.3%

DO: up 10.3% SKYE: down 16.0%

SKYE: down 16.0% PERI: down 28.6%

PERI: down 28.6% PCG: up 1.7%

PCG: up 1.7% X: down 0.2%

X: down 0.2% BITF: down 1.7%

BITF: down 1.7% ICCH: up 37.5%

ICCH: up 37.5% DNUT: up 5.4%

DNUT: up 5.4% PEGY: down 23.3%

PEGY: down 23.3% DK: down 2.1%

DK: down 2.1% ADBE: down 1.3%

ADBE: down 1.3% HBAN: down 6.0%

HBAN: down 6.0% AMD: down 3.4%

AMD: down 3.4% KKR: up 10.5%

KKR: up 10.5% STEP: up 8.0%

STEP: up 8.0% CVX: up 1.3%

CVX: up 1.3% MRO: up 1.9%

MRO: up 1.9% WMB: up 1.8%

WMB: up 1.8% AAPL: down 0.8%

AAPL: down 0.8% NEM: up 1.0%

NEM: up 1.0% ABX: up 1.1%

ABX: up 1.1% SSW: up 2.5%

SSW: up 2.5% FNV: up 1.8%

FNV: up 1.8% HON: up 0.5%

HON: up 0.5% NFBK: down 10.6%

NFBK: down 10.6% CE: down 1.5%

CE: down 1.5% CNX: up 2.4%

CNX: up 2.4% EQT: up 1.4%

EQT: up 1.4% NEXT: up 1.5%

NEXT: up 1.5% TELL: up 13.2%

TELL: up 13.2% NDX

NDX CEG

CEG LRCX

LRCX DDOG

DDOG MU

MU ILMN

ILMN ADP

ADP KHC

KHC PEP

PEP AVGO, with a market cap of $650 billion, ranks as the second-largest chipmaker and the eighth-largest U.S. company overall.

AVGO, with a market cap of $650 billion, ranks as the second-largest chipmaker and the eighth-largest U.S. company overall. QCOM

QCOM ADI

ADI MRVL

MRVL MCHP

MCHP MPWR

MPWR ON

ON DXY, making their products more expensive in emerging markets in Asia and Latin America.

DXY, making their products more expensive in emerging markets in Asia and Latin America.  DBA is a popular option for those looking to gain exposure to agricultural commodities. The ETF invests in a basket of agricultural resources such as corn, soybeans, wheat, sugar, cocoa, coffee, cotton, and feeder cattle, offering investors diverse commodity exposure and a hedge against inflation.

DBA is a popular option for those looking to gain exposure to agricultural commodities. The ETF invests in a basket of agricultural resources such as corn, soybeans, wheat, sugar, cocoa, coffee, cotton, and feeder cattle, offering investors diverse commodity exposure and a hedge against inflation.  ZTS, Bayer

ZTS, Bayer  BAYRY, Nutrien

BAYRY, Nutrien  NTR, and Corteva

NTR, and Corteva  CTVA, which account for 35.8% of the fund. While the majority of these holdings operate in developed markets, it also offers some exposure to emerging markets, such as Brazil and Malaysia.

CTVA, which account for 35.8% of the fund. While the majority of these holdings operate in developed markets, it also offers some exposure to emerging markets, such as Brazil and Malaysia.  ADM, Nutrien, and Lamb Weston

ADM, Nutrien, and Lamb Weston  LW, which together account for 45% of the ETF's weight.

LW, which together account for 45% of the ETF's weight.

ASML

ASML PDD

PDD GOOG

GOOG WBA

WBA CMCSA

CMCSA CHTR

CHTR XLI was the top performer for the day, up 1.1%, while the Utilities Select Sector SPDR Fund

XLI was the top performer for the day, up 1.1%, while the Utilities Select Sector SPDR Fund  XLU was the laggard with a flat performance.

XLU was the laggard with a flat performance. RDDT are indicated to open at $50-$52, in their first day of trading.

RDDT are indicated to open at $50-$52, in their first day of trading. SCS (down over 10%) and Five Below, Inc.

SCS (down over 10%) and Five Below, Inc.  FIVE (down about 15%), Accenture plc

FIVE (down about 15%), Accenture plc  ACN (down 8%), Winnebago Industries, Inc.

ACN (down 8%), Winnebago Industries, Inc.  WGO (up over 5%) and Shoe Carnival, Inc.

WGO (up over 5%) and Shoe Carnival, Inc.  SCVL (up nearly 7%), Darden Restaurants, Inc.

SCVL (up nearly 7%), Darden Restaurants, Inc.  DRI (down 6%).

DRI (down 6%). FDX, Lululemon Athletica Inc.

FDX, Lululemon Athletica Inc.  LULU, NIKE, Inc.

LULU, NIKE, Inc.  NKE and Worthington Steel, Inc. WWS.

NKE and Worthington Steel, Inc. WWS. BTBT and Coinbase Global Inc.

BTBT and Coinbase Global Inc.  SNOW tumbled nearly 20%, after the company announced that CEO Frank Slootman has decided to retire from his role as CEO. The AI-related company saw its revenue and earnings beating Wall Street’s analyst predictions last quarter.

SNOW tumbled nearly 20%, after the company announced that CEO Frank Slootman has decided to retire from his role as CEO. The AI-related company saw its revenue and earnings beating Wall Street’s analyst predictions last quarter. HRL rose over 13%, marking the highest daily performance among S&P 500 stocks, after the company unveiled better-than-expected results last quarter.

HRL rose over 13%, marking the highest daily performance among S&P 500 stocks, after the company unveiled better-than-expected results last quarter. MNST, up 5.7%, Celsius Holdings Inc.

MNST, up 5.7%, Celsius Holdings Inc.  CELH, up 19%, Okta Inc.

CELH, up 19%, Okta Inc.  OKTA, up 19%, Hayward Holdings Inc.

OKTA, up 19%, Hayward Holdings Inc.  HAYW, up 15%, Natera Inc.

HAYW, up 15%, Natera Inc.  NTRA, up 12%, The Chemours Company

NTRA, up 12%, The Chemours Company  CC, down 31%, DoubleVerify Holdings Inc.

CC, down 31%, DoubleVerify Holdings Inc.  DV, down 17%, AMC Entertainment Holdings Inc.

DV, down 17%, AMC Entertainment Holdings Inc.  AMC.

AMC. ADSK, Cooper Companies, Inc. CCOO, Fisker, Inc.

ADSK, Cooper Companies, Inc. CCOO, Fisker, Inc.  FSR, Zscaler, Inc.

FSR, Zscaler, Inc.  ZS, Hewlett Packard Enterprises Company

ZS, Hewlett Packard Enterprises Company  HPE, NetApp, Inc.

HPE, NetApp, Inc.  NTAP and SoundHound AI, Inc. (NASDAQ:SOUND).

NTAP and SoundHound AI, Inc. (NASDAQ:SOUND). AI jumped 24% to a six-month high on Thursday after the AI software firm delivered third-quarter results ahead of Wall Street expectations and narrowed its full-year revenue forecast on strong enterprise demand.

AI jumped 24% to a six-month high on Thursday after the AI software firm delivered third-quarter results ahead of Wall Street expectations and narrowed its full-year revenue forecast on strong enterprise demand. BBAI, Guardforce AI

BBAI, Guardforce AI  GFAI, Arm Holdings

GFAI, Arm Holdings  ARM and Nvidia

ARM and Nvidia  SOUN climbing 9% ahead of its fourth-quarter results due after markets close.

SOUN climbing 9% ahead of its fourth-quarter results due after markets close. PANW

PANW TTD

TTD NXPI

NXPI WDAY

WDAY AMGN

AMGN EA

EA TTWO

TTWO CTSH: down 0.2%

CTSH: down 0.2% ROKU: down 22.2%

ROKU: down 22.2% HTOO: up 134.2%

HTOO: up 134.2% TOST: up 16.5%

TOST: up 16.5% BE: down 18.5%

BE: down 18.5% THS: down 14.7%

THS: down 14.7% SRPT: up 8.5%

SRPT: up 8.5% DLR: down 7.4%

DLR: down 7.4% LAD: down 2.2%

LAD: down 2.2% PAG: down 1.1%

PAG: down 1.1% ABG: down 1.4%

ABG: down 1.4% AN: down 0.2%

AN: down 0.2% DNLI: down 6.7%

DNLI: down 6.7% HRT: up 9.4%

HRT: up 9.4% GE: up 0.9%

GE: up 0.9% DASH: down 8.2%

DASH: down 8.2% PPL: up 0.9%

PPL: up 0.9% KNSL: up 17.4%

KNSL: up 17.4% KNTE: up 11.9%

KNTE: up 11.9% DTM: up 4.2%

DTM: up 4.2% BIO: up 8.6%

BIO: up 8.6% PLCE: up 9.9%

PLCE: up 9.9% RIO: up 2.9%

RIO: up 2.9% BHP: up 1.8%

BHP: up 1.8% SCCO: up 1.7%

SCCO: up 1.7% HOOD: up 4.9%

HOOD: up 4.9% AMN: down 18.6%

AMN: down 18.6%

MDB

MDB PYPL

PYPL MRNA

MRNA DXCM

DXCM FI, Carrier Global

FI, Carrier Global  CARR, Spotify Technology

CARR, Spotify Technology  SPOT, and GE HealthCare Technologies

SPOT, and GE HealthCare Technologies  GEHC were among the companies that reported their latest financial results Tuesday.

GEHC were among the companies that reported their latest financial results Tuesday. CMG, Ford Motor

CMG, Ford Motor  SNAP are among the companies scheduled to report after the closing bell.

SNAP are among the companies scheduled to report after the closing bell. META, up 20.8%

META, up 20.8% AMZN, up 7.9%

AMZN, up 7.9% EW, up 7.6%

EW, up 7.6% GEN, down 13.5%

GEN, down 13.5% ENPH, down 4.3%

ENPH, down 4.3% DPSI, up 16.6%

DPSI, up 16.6% DECK, up 16%

DECK, up 16% WNS, down 15.7%

WNS, down 15.7% ATUS, down 15.3%

ATUS, down 15.3% MCAF, up 46.8%

MCAF, up 46.8% GNPX, down 22.3%

GNPX, down 22.3% SHLTN, down 21%

SHLTN, down 21% NYCB: up 6.3%

NYCB: up 6.3% CI: up 6%

CI: up 6% PINS: up 4.8%

PINS: up 4.8% CLX: up 5.6%

CLX: up 5.6% MAT: up 3.3%

MAT: up 3.3% SKX: down 9.6%

SKX: down 9.6% RVNC: up 0.7%

RVNC: up 0.7% PIPR: up 5.4%

PIPR: up 5.4% LYB: down 2.2%

LYB: down 2.2% HIG: up 3.5%

HIG: up 3.5% ABBV: up 0.6%

ABBV: up 0.6% AON: down 2.5%

AON: down 2.5% IMO: up 0.9%

IMO: up 0.9% VRTX: down 1.5%

VRTX: down 1.5%

沒有留言:

發佈留言